Relationship with IRS

Last Updated: May 20, 2024

An official website of the United States government.

The .gov means it’s official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information, make sure you’re on a federal government site.

The site is secure.

The https:// ensures that you are connecting to the official website and that any information you provide is encrypted and transmitted securely.

Last Updated: May 20, 2024

IRS Background.

Divisions. The IRS has four operating divisions: Wage and Investment, Small Business/Self-Employed, Large Business and International, and Tax Exempt and Government Entities (TE/GE). The Department coordinates primarily with the IRS TE/GE division, which services employee plans, tax-exempt organizations, and government entities.

EP Examinations and the geographic examination areas:

| Office | Covered States |

|---|---|

| Cincinnati, OH | Pennsylvania, North & South Carolina, Maryland, DC, Ohio, Virginia, West Virginia |

| Chicago, IL | Missouri, Kentucky, Wisconsin, Michigan, Minnesota, Indiana, Illinois, Iowa, South Dakota, North Dakota, Nebraska |

| Plantation, FL | Texas, Louisiana, Florida, Arkansas, Kansas, Georgia, Tennessee, Oklahoma, Alabama, Arizona |

| Brooklyn, NY | New York, New Jersey, Massachusetts, Connecticut, Maine, New Hampshire |

| Portland, OR | Colorado, California, Oregon, Washington, New Mexico, Utah, Arizona, Nevada |

Special Function EP Offices

| Office | Function |

|---|---|

| Richmond, VA | This group reviews all EP related referrals from DOL |

| Baltimore, MD | Functional Assignment Coordinator (FAC) |

EP Contact Information. Employee Plan Customer Service(1):

Internal Revenue Service

Attn: EP Customer Service Manager

P.O. Box 2508

Cincinnati, OH 45201

(P) 877-829-5500

Minimum Standards Scope.

Responsibility. The Department and the IRS both have responsibilities for benefit plans based on ERISA Title I part 2 (participation, vesting, and benefit accrual for retirement plans) and part 3 (funding defined benefit pension plans, money purchase pension plans and target benefit plans). Department Investigator/Auditors must determine if the benefit plan is subject to parts 2 and 3. If so, it may be possible to work with the IRS. Section 22, below, provides information on referrals between the agencies. If an investigator believes a violation of Title I, part 2 or part 3 may also violate part 4, the region should consult with OE prior to making a final determination.

Vesting. ERISA Section 203 establishes minimum vesting standards for employer contributions. This means that a plan can only require an employee to work for a certain time before the employer contributions vest. A plan must adhere to one of two vesting schedules outlined in Section 203(a)(2).(2)

If an employee contributes to the plan, then those contributions are vested immediately (i.e., as soon as the contributions are made). Section 204(c) provides rules for separating the benefits derived from employee contributions and those derived from employer contributions.

Failure of Employer to Make Required Contributions to a Plan Maintained by more than one Employer. A pension plan maintained by more than one employer must credit an employee for service towards benefit accrual (and eligibility for participation and vesting) even if the employer fails to make required contributions to the plan.(10)

Any Department referral to the IRS relating to violations of this nature should contain information regarding the plan's tax qualification status, including the dates of the plan's most recent submission of a determination request, and the IRS response, if any. The referral should also indicate whether there is express language in the plan's documents on the plan's denial of benefits.

IRC Section 6104 Information. The RO should not request IRC Section 6103(l)(2) information that is already authorized to be disclosed under IRC Section 6104.

IRC Section 6104 provides that any application for tax-qualified status, tax-exempt status, or papers submitted in support of any such applications is open for public inspection.(15) However, if a plan has 25 or fewer participants, this right of public inspection is open only to a plan participant. Section IRC Section 6104 specifies places and times for public inspection. Materials or documents regarding an individual's compensation are not open to public inspection.

In order for the IRS and DOL to fulfill the mandates of the Employee Retirement Income Security Act of 1974 (ERISA) Sections 3003 and 3004 and in accordance with ERISA Section 506, the IRS and DOL have executed the Internal Revenue Service/Department of Labor Coordination Agreement (Agreement).

The agreement reflects changes resulting from Implementation of the IRS FTI Secure Data Transfer (SDT) Tool, and other revisions identified from the agencies’ experiences under prior agreements.

Although an essential component of the Agreement is timely coordination and emphasis on the need to eliminate duplicative investigative efforts, the agencies recognize there may be situations that require both agencies to become involved. The IRS and DOL agree to identify past situations where both agencies have had an examination/investigation on the same subject and to determine when it may be beneficial for the agencies and the public for examinations/investigations to be conducted jointly.

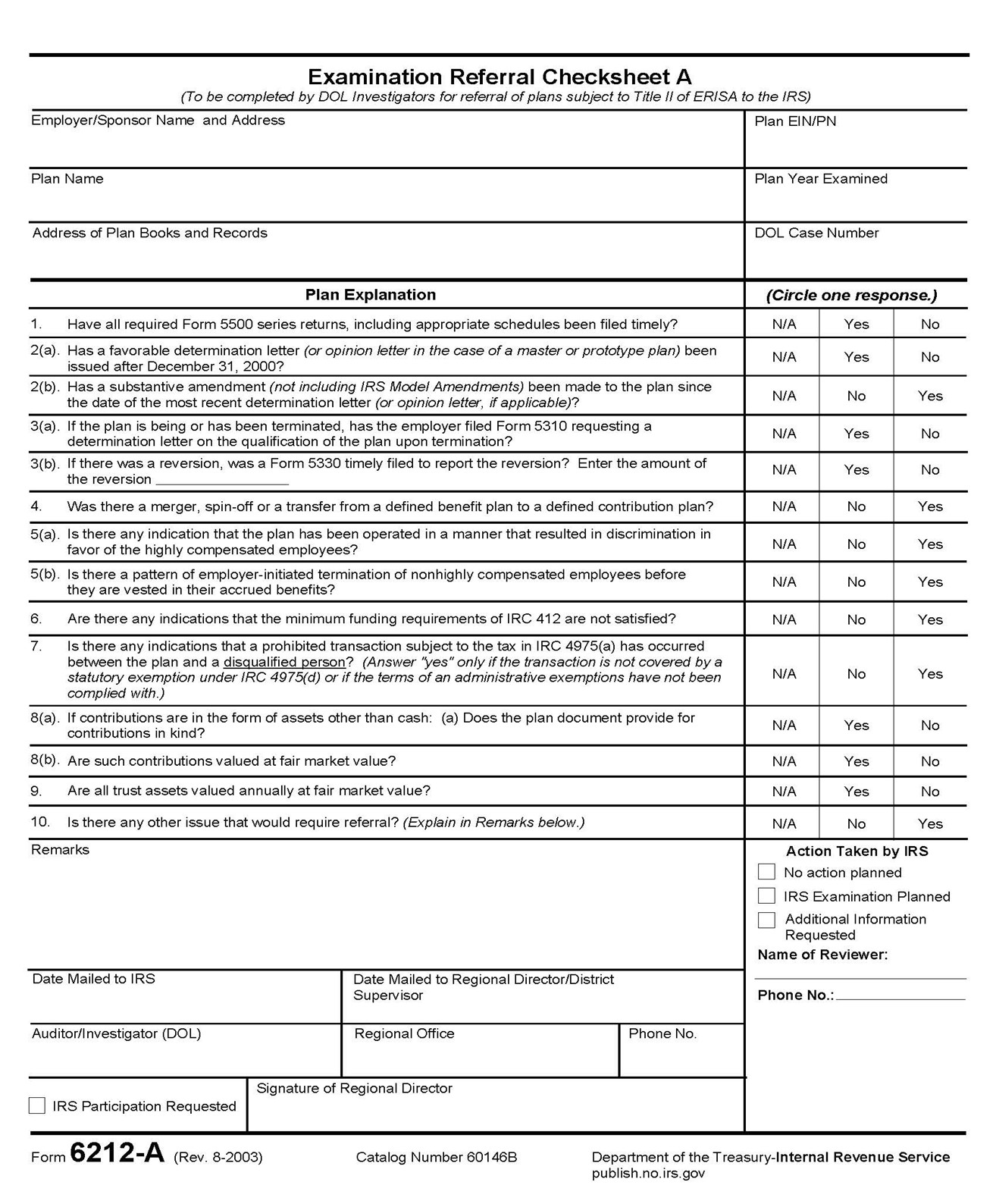

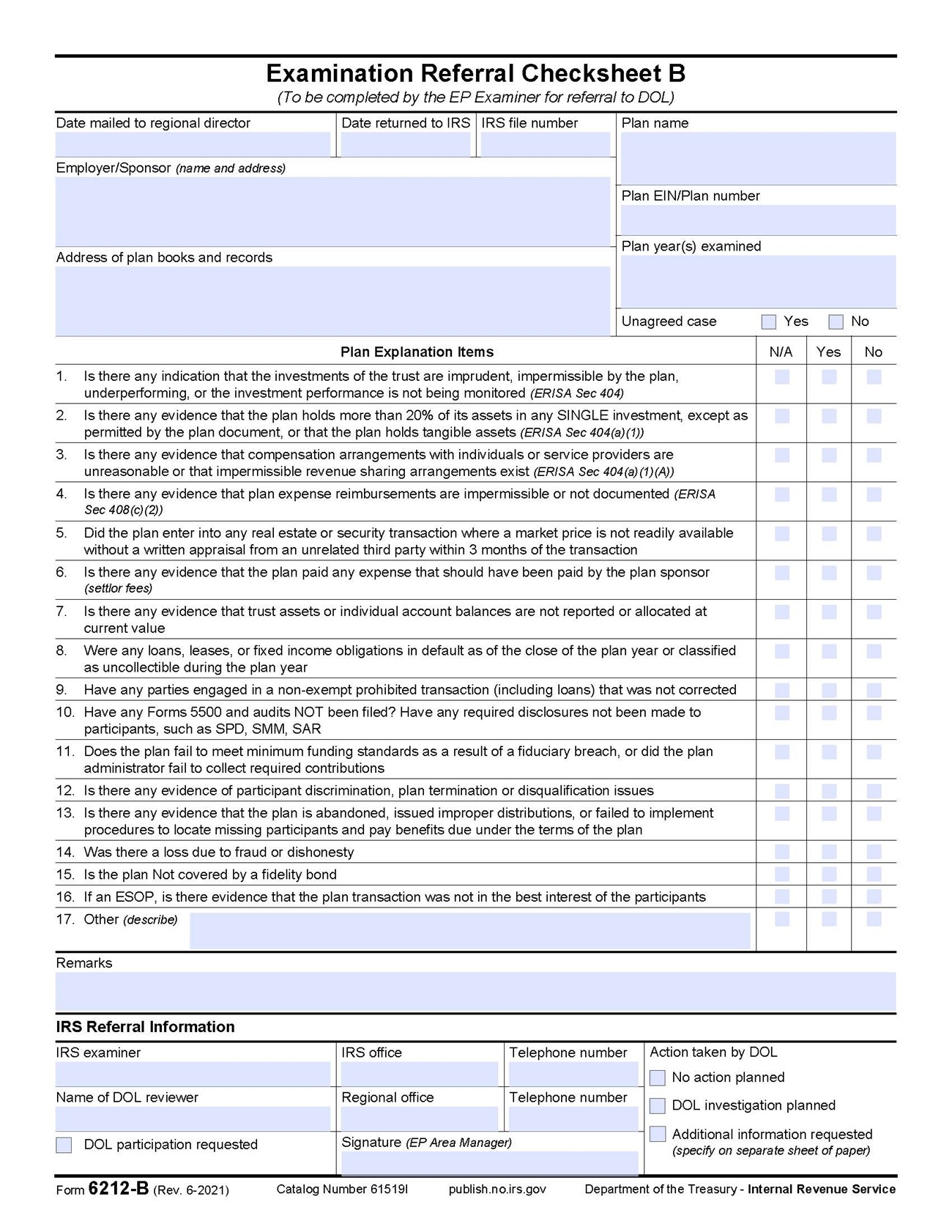

DOL will continue to refer Form 6212-A to IRS for welfare benefit plans and pension benefit plans in accordance with the requirements of Article II, D., of the Agreement. IRS will continue to make referrals to DOL on Form 6212-B in accordance with the requirements of Article II, C. of the Agreement.

Employee Plans is a function of the TE/GE Operating Division of the IRS. The Director, EP Examinations supervises five Area Managers located around the country. The Director, Compliance, Planning and Classification supervises the Senior Managers of Classification and Case Assignment, Issue ID and Planning and Monitoring. Referrals made by EBSA personnel are now made to the Classification and Case Assignment area of TE/GE Compliance, Planning and Classification through the SDT Tool, which was implemented in 2020. In accordance with Article V. C. of the Agreement, representatives of the IRS and DOL will meet at a minimum of semi-annually.

/s/ June 26, 2023

Eric D. Slack

Director, Employee Plans

/s/ June 14, 2023

Timothy D. Hauser

Deputy Assistant Secretary for Program Operations

Employee Benefits Security Administration

General

For the agencies to avoid unnecessary duplication in examinations, the Department of Labor, Employee Benefits Security Administration (EBSA) Regional Offices or the National Office will notify the IRS Classification and Case Assignment area monthly of the names of pension benefit plans selected for civil investigation. Regional Offices may individually send case listings to the Classification and Case Assignment area, they may collaborate and send one list that includes the names of all pension benefit plans selected for civil investigation, or the National Office may send one listing on behalf of all regions. These notifications, referred to as “Open Transmittal Reports” shall be sent via email to tege.ep.classification@irs.gov or electronically via the SDT monthly. Nothing contained in this agreement shall preclude the agencies from agreeing to use special procedures, including joint or concurrent investigations/examinations in appropriate cases.

EBSA Action After Positive Feedback

Generally, EBSA and IRS will collaborate on investigations if IRS advises the Regional Director that the investigation would be duplicative. If IRS has selected a plan for examination but has not yet initiated contact with the plan, the EBSA Regional Office and the EP Examinations Area Office with jurisdiction over the plan will decide which agency will examine/ investigate the plan. Any jurisdictional disputes will be resolved in accordance with section A.6. of Part II below.

Applicability

The following procedures apply to all cases received by IRS Appeals Offices involving examinations of employee benefit plans within the meaning of section A.2. of Part II.

Notification to EBSA

The applicable Appeals Area Director (or designee) will notify, in writing, the EBSA Regional Director's Office as listed in Exhibit B that an employee plans case has been received in their office. To ensure that notice has been given to DOL as required by Sections 4971(d) and 4975(h) of the Internal Revenue Code, the Appeals Office shall follow the procedures of B. and C. of this part.

Final Resolution

If the Appeals Area Director and the EBSA Regional Director are unable to reach agreement regarding disposition of the case, the matter will be forwarded to the National Chief, Appeals, to coordinate final resolution with the Director, EBSA Office of Enforcement, DOL.

Litigation Involving DOL and Relating to Employee Benefit Plans

The Solicitor of Labor (or designee) will notify the TEGEDC, and the Director, EP Examinations T:EP:E, when it is determined that litigation by DOL relating to employee benefit plans is warranted. Copies of the proposed complaint will be furnished to the TEGEDC and to the Department of Justice for review.

Referral Reconciliations

IRS and DOL will conduct formal referral reconciliations twice yearly. Agencies are not precluded from communicating more frequently on referrals as needed.

Excise Taxes

The FAC, upon closure of an examination initiated as the result of a referral from DOL, will forward to the EBSA Regional Results Sheet indicating the amount of Internal Revenue Code section 4971(a) and/or (b) or 4975 proposed or assessed excise tax. If the IRS does not propose or assess excise taxes, then the reasons will be entered in the “Remarks” section of Form 6212-A.

Resolution of Disputes

IRS EP Examinations and DOL National Office personnel will meet at least semiannually to resolve any referrals on which the appropriate enforcement action is in dispute. These meetings will also be used as a medium for discussions of issues encountered by EBSA Regional Offices and IRS EP Examinations in following the provisions of this Agreement.

Work Plan and Initiatives

The IRS Director of EP Examinations (or Representative) and the EBSA’s Director of the Office of Enforcement (or Representative) will meet at the start of each fiscal year but no later than October 31st to review work plan and initiatives for the fiscal year (i.e., programs, data mining, projects).

Local Contact List

IRS-EP Examinations and DOL-EBSA Local Contact List will be updated annually. Agencies are not precluded from updating the list more frequently, as needed.

IRS Disclosure

In general, IRS is prohibited from disclosing any tax information to anyone outside of the IRS. IRC section 6103 lists the exceptions to this general rule. IRC section 6103(l)(2) allows the IRS to furnish information to the DOL and PBGC for the enforcement of Titles I and IV of ERISA. This includes requests for tax returns and tax return information Disclosures under IRC section 6103(l)(2) are required to be accounted for per IRC section 6103(p)(3)(A). This is accomplished by TE/GE by use of Form 5466-B.

| Office | Covered States | Area Manager | Main Phone |

|---|---|---|---|

| Cincinnati, OH | Pennsylvania, North & South Carolina, Maryland, DC, Ohio, Virginia, West Virginia | Ryan McDonald | 513-975-6470 |

| Chicago, IL | Missouri, Kentucky, Wisconsin, Michigan, Minnesota, Indiana, Illinois, Iowa, South Dakota, North Dakota, Nebraska | John Wright | 312-292-4583 |

| Plantation, FL | Texas, Louisiana, Florida, Arkansas, Kansas, Georgia, Tennessee, Oklahoma, Alabama, Arizona | Sharon Gowans | 954-991-4174 |

| Brooklyn, NY | New York, New Jersey, Massachusetts, Connecticut, Maine, New Hampshire | Janet Mak | |

| Portland, OR | Colorado, California, Oregon, Washington, New Mexico, Utah, Arizona, Nevada | Stephanie Harris | 503-265-3731 |

| Richmond, VA | His group reviews all EP related referrals from DOL | Christopher Huxtable | 804-916-8211 |

| Baltimore, MD | Functional Assignment Coordinator (FAC) | Jonathan Limes | 443-853-5520 |

| Office | Regional Director | Main Phone |

|---|---|---|

| Atlanta | Crystal Coleman 61 Forsyth St, SW, Ste 7B54 Atlanta, GA 30303 | 404-302-3900 Fax: 404-302-3975 |

| Boston | Carol Hamilton JFK Federal Bldg. 15 Sudbury St, Rm 575 Boston, MA 02203 | 617-565-9600 Fax: 617-565-9666 |

| Chicago | Ruben Chapa John C. Kluczynski Federal Bldg. 230 S. Dearborn Street, Ste 2160 Chicago, IL 60604 | 312-353-0900 Fax: 312-353-1023 |

| Cincinnati | Joe Rivers 1885 Dixie Hwy, Ste 210 Ft. Wright, KY 41011-2664 | 859-578-4680 Fax: 859-578-4688 |

| Dallas | Deborah Perry 525 South Griffin St, Rm 900 Dallas, TX 75202-5025 | 972-850-4500 Fax: 214-767-1055 |

| Kansas City | Mark Underwood 2300 Main St, Ste 11093 Kansas City, MO 64108 | 816-285-1800 Fax: 816-285-1888 |

| Los Angeles | Crisanta Johnson 35 N. Lake Ave., Ste 300 Pasadena, CA 91101 | 626-229-1000 Fax: 626-229-1098 |

| New York | Thomas Licetti 201 Varick Street, Room 746 New York, NY 10014 | 212-607-8600 Fax: 212-607-8611 |

| Philadelphia | Cristina O’Brien 1835 Market Street, 21st Floor Mailstop EBSA/21 Philadelphia, PA 19103-2968 | 202-693-8747 Fax: 215-861-5347 |

| San Francisco | Klaus Placke 90 7th St, Ste 11-300 San Francisco, CA 94103 | 415-625-2481 Fax: 415-625-2450 |

Prepared by the President and transmitted to the Senate and the House of Representatives in Congress assembled, August 10, 1978, pursuant to the provisions of Chapter 9 of Title 5 of the United States Code.

Except as otherwise provided in Sections 104 and 106 of this plan, all authority of the Secretary of Labor to issue the following described documents pursuant to the statutes hereinafter specified is hereby transferred to the Secretary of the Treasury:

Except as otherwise provided in Section 105 of this Plan, all authority of the Secretary of the Treasury to issue the following described documents pursuant to the statutes hereinafter specified is hereby transferred to the Secretary of Labor:

In the case of fiduciary actions which are subject to Part 4 of Subtitle B of Title I of ERISA, the Secretary of the Treasury shall notify the Secretary of Labor prior to the time of commencing any proceedings to determine whether the action violates the exclusive benefit rule of subsection 401(a) of the Code, but not later than prior to issuing a preliminary notice of intent to disqualify under that rule, and the Secretary of the Treasury shall not issue a determination that a plan or trust does not satisfy the requirements of subsection 401(a) by reason of the exclusive benefit rule of subsection 401(a), unless within 90 days after the date on which the Secretary of the Treasury notifies the Secretary of Labor of pending action, the Secretary of Labor certifies that he has no objection to the disqualification or the Secretary of Labor fails to respond to the Secretary of the Treasury. The requirements of this paragraph do not apply to the case of any termination or jeopardy assessment under sections 6851 or 6861 of the Code that has been approved in advance by the Commissioner of Internal Revenue, or, as delegated, the Assistant Commissioner for Employee Plans and Exemption Organizations.

The transfers provided for in Section 101 of this Plan shall not affect the ability of the Secretary of Labor, subject to the provisions of Title III of ERISA relating to jurisdiction, administration, and enforcement, to engage in enforcement under Section 502 of ERISA or to exercise the authority set forth under Title III of ERISA, including the ability to make interpretations necessary to engage in such enforcement or to exercise such authority. However, in bringing such actions and in exercising such authority with respect to Parts 2 and 3 of Subtitle B of Title I of ERISA and any definitions for which the authority of the Secretary of Labor is transferred to the Secretary of the Treasury as provided in Section 101 of this Plan, the Secretary of Labor shall be bound by the regulations, rulings, opinions, variances, and waivers issued by the Secretary of the Treasury.

The transfers provided for in Section 102 of this Plan shall not affect the ability of the Secretary of the Treasury, subject to the provisions of Title III of ERISA relating to jurisdiction, administration, and enforcement, (a) to audit plans and employers and to enforce the excise tax provisions of subsections 4975(a) and 4975(b) of the Code, to exercise the authority set forth in subsections 502(b)(1) and 502(h) of ERISA, or to exercise the authority set forth in Title III of ERISA, including the ability to make interpretations necessary to audit, to enforce such taxes, and to exercise such authority; and (b) consistent with the coordination requirements under Section 103 of this Plan, to disqualify, under section 401 of the Code, a plan subject to Part 4 of Subtitle B of Title I of ERISA, including the ability to make the interpretations necessary to make such disqualification. However, in enforcing such excise taxes, and, to the extent applicable, in disqualifying such plans the Secretary of the Treasury shall be bound by the regulations, rulings, opinions, and exemptions issued by the Secretary of Labor pursuant to the authority transferred to the Secretary of Labor as provided in Section 102 of this Plan.

On or before April 30, 1980, the President will submit to both Houses of the Congress an evaluation of the extent to which this Reorganization Plan has alleviated the problems associated with the present administrative structure under ERISA, accompanied by specific legislative recommendations for a long-term administrative structure under ERISA.

So much of the personnel, property, records, and unexpended balances of appropriations, allocations and other funds employed, used, held, available, or to be made available in connection with the functions transferred under this Plan, as the Director of the Office of Management and Budget shall determine, shall be transferred to the appropriate agency, or component at such time or times as the Director of the Office of Management and Budget shall provide, except that no such expended balances transferred shall be used for purposes other than those for which the appropriation was originally made. The Director of the Office of Management and Budget shall provide for terminating the affairs of any agencies abolished herein and for such further measures and dispositions as such Director deems necessary to effectuate the purpose of this Reorganization Plan.

The provisions of this Reorganization Plan shall become effective at such time or times, on or before April 30, 1979, as the President shall specify, but not sooner than the earliest time allowable under Section 906 of Title 5, United States Code.

The Health Insurance Portability and Accountability Act of 1996 ("HIPAA"), Pub. L. No. 104-191, was enacted on August 21, 1996. Titles I and IV of HIPAA amended the Internal Revenue Code, the Employee Retirement Income Security Act of 1974, and the Public Health Service Act to add provisions to improve access, portability, and continuity of health insurance coverage in the group and individual health insurance markets.

Section 104 of HIPAA directs the Secretary of the Treasury, the Secretary of Labor, and the Secretary of Health and Human Services to enter into an interagency memorandum of understanding. Section 104 requires that the memorandum of understanding ensure that regulations, rulings, and interpretations relating to the changes made by Subtitle A of Title I and section 401 of Title IV of HIPAA over which two or more Secretaries have responsibility ("shared provisions") are administered so as to have the same effect at all times. Section 104 also requires the coordination of policies relating to enforcing the shared provisions in order to avoid duplication of enforcement efforts and to assign priorities in enforcement. This memorandum of understanding (MOU) is adopted pursuant to section 104 of HIPAA.

This MOU formally establishes an interagency agreement among the Secretary of the Treasury, the Secretary of Labor, and the Secretary of Health and Human Services to ensure coordination in the manner and for the purposes set forth in section 104 of HIPAA. The Departments also intend to follow the process set forth in this MOU, to the extent appropriate, with regard to interpretations and enforcement of the provisions of the Newborns' and Mothers' Health Protection Act of 1996, the Mental Health Parity Act of 1996, and Subsequent Legislation. In addition, the Departments of Labor and HHS agree to follow the process set forth in this MOU, to the extent appropriate, with regard to interpretations and enforcement of the provisions of the Women's Health and Cancer Rights Act of 1998.

This MOU is entered pursuant to the authority set forth in section 104 of HIPAA, Pub. L. No. 104-191.

Subtitle A of Title I and section 401 of Title IV of HIPAA are intended to improve the availability of private health insurance by increasing portability, access, and renewability in the group market. HIPAA establishes limits on the imposition of preexisting condition exclusions and generally prohibits group health plans and health insurance issuers from discriminating against individuals based on health status when determining eligibility to enroll in a group health plan or to obtain related insurance or in deciding the amount of premium to be charged to similarly situated individuals. Employers may not be denied continued access to multiemployer plans, or multiple employer welfare arrangements, except for certain reasons set forth in HIPAA.

HIPAA and Related Acts amended three federal statutes: the Code, administered by the Treasury through IRS; ERISA, administered by DOL through PWBA; and the PHS Act, administered by HHS through HCFA. Under the Code, as amended by HIPAA and Related Acts, the Treasury has authority over group health plans (including church plans) and their sponsors, and IRS enforced the requirements of HIPAA and Related Acts through the imposition of an excise tax. Under ERISA, as amended by HIPAA and Related Acts, DOL has increased authority over group health plans that are subject to Part 7 of subtitle B of Title I of ERISA. Health insurance issuers offering health insurance coverage in connection with such plans are also subject to Part 7. However, in accordance with the provisions of HIPAA, only participants and beneficiaries (and not DOL) may bring an enforcement action against health insurance issuers under Part 7.

Under the PHA Act, as amended by HIPAA and Related Acts, HCFA has authority over health insurance issuers and nonfederal governmental plans. If a State fails to substantially enforce Parts A and B of Title XXVII of the PHS Act, or requests that HCFA enforce the provisions or requirements, HCFA enforces the group and individual market requirements by imposing a civil monetary penalty on issuers that fail to comply with HIPAA's requirements in that State.

There are differences in some of the amendments that HIPAA and Related Acts made to the three statutes. In some instances, changes were made to only one of the federal statutes with no counterpart in the other two statutes. Section 104 of HIPAA requires the Secretaries of the Treasury, Labor, and HHS to coordinate in the areas of parallel responsibility relating to the share provisions of HIPAA.

The Departments agree to assign representatives to work closely to ensure that all Interpretations, Regulations, and enforcement strategies relating to shared provisions of Subtitle A of Title I and section 401 of Title IV of HIPAA and Related Acts will be developed and implemented in a coordinated manner. All such Interpretations, Regulations and enforcement strategies will be administered in a manner that promotes consistency in effect, that avoids duplication of enforcement efforts, and that reflects consideration of the appropriate priorities in enforcement.

In this regard, the Departments will continue to work together closely through regular joint meetings and frequent consultation, consistent with the process (i.e., by mutual consent) that has been used in developing existing Regulations and Interpretations under HIPAA and Related Acts. Similarly, DOL and HHS will continue to work together closely through regular joint meetings and frequent consultation to develop Regulations and Interpretations under WHCRA.

In order to further effectuate this coordination, the Treasury, IRS, DOL, and HHS each will name a "Department Designee" to serve on a Coordinating Committee. The Committee's task will be to ensure the identification and coordination of policies involving areas of shared responsibility under HIPAA and Related Acts to maintain consistency in the application of these provisions that amend the Code, ERISA, and the PHS Act.

The Committee also will take steps to maximize the efficiency of Agency enforcement efforts, including developing the terms of further agreement(s), as necessary. The Committee members shall meet, quarterly, or at such times as they may agree, to review and discuss relevant pending Regulations and Interpretations to evaluate whether the position(s) set forth therein reflect a coordinated position. Committee meetings will be held at locations agreed to by the Committee members. Upon agreement of the Committee members, such meetings may be held by conference call. Each Department will assume the costs associated with the participation of its respective Committee members.

Timely and prompt consensus will be sought in the development and administration of all interpretations affected by this MOU. Any Department Designee can bring any matter subject to the MOU before the Committee. The Department Designees serving on the Committee will attempt to reach consensus on issues within 45 days (except in unusual circumstances) after such issues have been formally presented (including a written summary) at a meeting of the Committee. If consensus on particular issues is reached by the members of the Committee, appropriate clearance will be initiated within each Department.

Generally, the Departments intend to continue the current informal arrangements that have developed for cooperation and collaboration in the handling of inquiries arising under HIPAA, MHPA, NMHPA, and WHCRA. In addition, pursuant to Section 104(2) of HIPAA and this MOU, the Committee, and any appropriate individuals designated by the Agencies or Departments, shall develop a coordinated enforcement strategy that avoids duplication of enforcement efforts and assigns priorities in enforcement. The Agencies or Departments shall first designate, within six months of the execution of this MOU, individuals who are to work with the Committee in developing the enforcement strategy. This group shall also devise a written operational agreement for the sharing of information that is related to enforcement cases among the Departments. Moreover, the operational agreement may address procedures for the referral of cases, the development of audit checklists and training materials, and the coordination of public affairs information. The operational agreement may also describe the individuals within each Department who are responsible for implementing the sharing of information. Subject to applicable legal restrictions (including section 6103 of the Code), the Departments agree, absent exigent circumstances, to notify each other in writing (through the Department Designee) prior to the commencement of any administrative or judicial proceeding on matters within the scope of this MOU and to inform each other of the final action resulting from such proceeding.

Nothing in this section shall be construed to affect the enforcement authority that HIPAA or Related Acts confers on any Department, including enforcement concerning a matter as to which a Department has given or received the information or notice described herein, nor shall this paragraph be construed to preclude the Departments from agreeing to different arrangements on a case by case basis.

The Departments agree that any information shared or disclosed pursuant to this MOU will be held in strict confidence and may be used only for purposes consistent with this MOU or as otherwise permitted by law. All requests by parties other than the Departments for disclosure of information shall be coordinated with the Agency that initially compiled or collected the information, provided that no Agency shall disclose information initially compiled by another Agency to the public without the approval of the appropriate Agency or Department unless the Agency is required by law to do so (e.g., Freedom of Information Act (FOIA), 5 U.S.C. 552; Federal Advisory Committee Act (FACA), 5 U.S.C. App. 2), in which event it will notify the appropriate Department or Agency in writing of its intent to disclose such information. Nothing in this MOU shall be deemed to confer rights on any party other than the Departments as a result of any act or omission by any Agency or Department with respect to its obligations under this MOU.

This MOU will become effective upon the date of the final signature and may be amended by written agreement of the undersigned. It will remain in effect until amended by the parties, or until terminated by any of the parties upon 30 days written notice to the other parties and, upon the agreement of the Departments, shall apply to Subsequent Legislation.

The appropriate Departmental officials will appoint their respective Department Designees to the Committee within 30 days after the signing of this MOU and will appoint any successors in a timely manner.

We, the undersigned, do hereby agree to the foregoing provisions of this MOU.

Dated: April 8, 1999.

Donald C. Lubick,

Assistant Secretary for Tax Policy, Department of the Treasury.

We, the undersigned, do hereby agree to the foregoing provisions of this MOU.

Dated: April 21, 1999.

Robert E. Wenzel,

Deputy Commissioner, Internal Revenue Service, Department of the Treasury.

We, the undersigned, do hereby agree to the foregoing provisions of this MOU.

Dated: March 17, 1999.

Richard M. McGahey,

Assistant Secretary, Pension and Welfare Benefits Administration, Department of Labor.

We, the undersigned, do hereby agree to the foregoing provisions of this MOU.

Dated: March 30, 1999.

Nancy-Ann Min DeParle,

Administrator, Health Care Financing Administration, Department of Health and Human Services.