Form LM-3 Common Reporting Errors

The Office of Labor-Management Standards (OLMS) enforces certain provisions of the Labor- Management Reporting and Disclosure Act (LMRDA), including reporting and disclosure requirements for labor unions, their officers and employees, employers, labor relations consultants, and surety companies. The LMRDA also requires, in part, that unions meet basic standards of fiscal responsibility. The purpose of this Compliance Tip is to help union officials and accountants who prepare the Form LM-3 (Labor Organization Annual Report) avoid some common reporting errors.

The six most common errors:

- All required information is not always entered in Item 23 (Rates of Dues and Fees).

- Insufficient details are provided for Items 10 – 18. When Items 10 – 18 are checked “Yes,” the filer is required to provide an explanation in Item 56 (Additional Information).

- All required information is not always entered in Item 24 (All Officers and Disbursements to Officers).

- All required information for Statement A (Assets and Liabilities) and Statement B (Receipts and Disbursements) is not always entered.

- Filers provide inadequate information for the Fidelity Bond (Item 20).

- Insufficient details are provided when cash does not reconcile.

Most of these reporting errors will be brought to your attention when you complete your validation process using the Electronic Forms System (EFS), which is mandatory for all filers. However, even though EFS will direct you to Item 56 to provide additional information if you check “Yes” for Items 10 – 18, it does not determine whether the additional information is adequate. Additionally, EFS will not automatically calculate your minimum bonding required (Item 20).

The following recommendations are made to help you prepare an accurate Form LM-3 Report:

1. Properly complete Item 23:

In Item 23, you must enter information on dues or fees in lines (a) through (d), even if the entry is a zero or “N/A.” In the following example, if regular monthly dues are $25.50 per month, and the initiation fees are a minimum of $50.00 and a maximum of $250.00 per member and there are no other transfer fees or work permits, the completed Item 23 should correspond to the example below.

Rates of Dues and Fees

|

Dues/Fees |

Amount |

Unit |

Minimum |

Maximum |

|---|---|---|---|---|

|

(a) Regular Dues/Fees |

$ 25.50 per |

Month |

N/A |

N/A |

|

(b) Initiation Fees |

N/A |

Member |

$50.00 |

$250.00 |

|

(c) Transfer Fees |

N/A |

|

N/A |

N/A |

|

(d) Work Permits |

N/A |

|

N/A |

N/A |

2. Properly sufficient detail for Items 10 - 18:

Another reporting error by Form LM-3 filers is when “Yes” is checked for Items 10 – 18, but filers do not provide the required detailed explanation in Item 56. In the following table, the required details from the Form LM-3 Instructions are spelled out in summary form for easy reference.

|

Item Number and |

Detail required in Item 56, if "Yes" checked |

|---|---|

|

10. Subsidiary Organization |

Provide the name, address and purpose of each subsidiary organization and indicate whether the information concerning its financial condition and operations are included in this Form |

|

11. Trusts or Funds |

Provide the name, address and purpose of each trust. If a report has been filed for the trust under the Employee Retirement Income Security Act (ERISA), report the ERISA file number and plan number, if any. |

|

12. Political Action Committee |

Provide the name of each political action committee (PAC) and |

|

13. Acquisition or Disposition of Assets |

Describe the manner in which your organization acquired or disposed of assets, such as donating office furniture or equipment to charitable organizations, trading in assets, writing off a receivable, or giving away other tangible or intangible property. Include the type of asset, its value, and the identity of the recipient or donor, if any. Also report the cost or other basis at which any acquired assets were entered on your organization’s books or the cost or other basis at which any assets disposed of were carried on your organization’s books. |

|

14. Audit or Review of the Books and Records |

Indicate whether the audit or review was performed by an outside accountant or a parent body auditor/representative. If it was performed by an outside accountant, provide the name of the accountant. Report any audit or review in which your organization’s books and records were examined to verify their accuracy and validity. |

|

15. Losses or Shortages |

Describe the loss or shortage in detail, including such information as the amount of the loss or shortage or a description of the property that was lost, how it was lost, and to what extent, if any, there has been an agreement to make restitution or any recovery by means of repayment, fidelity bond, insurance, or other means. |

|

16. Additional Positions of Officers |

For those officers paid $10,000 or more in salary from your organization and also paid $10,000 or more from another labor organization or employee benefit plan, list the name of each such officer, the name of the other labor organization(s) or benefit plan(s), and the officer’s position in the other labor organization(s) or employee benefit plan(s). |

|

17. Employees |

If any employee received more than $10,000 in gross salaries, allowances and other direct or indirect disbursements, report the name and position of each employee and the names of the other affiliated labor organizations which made disbursements to or on behalf of the employee. Also report the total disbursements made to each employee or on the employee’s behalf by your organization, including all salary and allowances (before any deductions) and other disbursements (including reimbursed expenses). |

|

18. Loans |

Report in Item 56 the name of each individual and business enterprise, the amount each individual owed at the end of the reporting period, and the amount loaned to each business enterprise during the reporting period. Also report in Item 56 the purpose, terms for repayment, and any security for each such loan. |

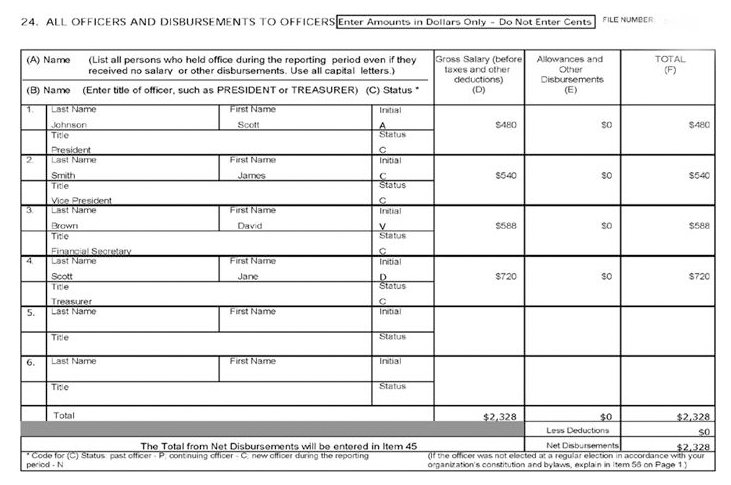

3. Properly Complete Item 24:

Item 24 (All Officers and Disbursements to Officers) requires reporting all the labor organization’s officers’ salaries and other direct and indirect disbursements during the reporting period. Columns (A) through (F) must be completed with an amount or zero. Item 24 should be completed as in the example below.

4. Properly complete Statements A and B:

EFS will validate Statement A (Assets and Liabilities) and Statement B (Receipts and Disbursements) only if all items are completed with an amount or zero. Blank entries are not permitted in Statements A and B.

Below is an example of an accurately completed Statement A and B.

5. Adequately Calculate Bonding:

If your organization had property and annual financial receipts that total more than $5,000, each of your organization’s officers, employees, and agents who handles funds or other property of your organization must be bonded. The amount of the bond must be at least 10% of the value of the funds handled by the individual during the last reporting period, up to a maximum bond of $500,000.

Your organization must report the correct bonding amount in Form LM-3, Item 20 (Fidelity Bond). The amount reported must cover the fiscal year included in the report, not the amount in place at the time of submitting the report. For example, if you file your FY 19 report in March 2020, you must report the bond in place during FY 19, not any increase obtained during 2020.

Please note that the amount of bonding must be calculated each year, based on the amount of funds handled in the prior fiscal year, and updated if necessary. Using the Bonding Computation Worksheet will enable an accurate calculation. If based on the calculation an increase is necessary, the surety company must be contacted to update the policy and the updated amount reported in Item 20 (Fidelity Bond). Alternatively, certain labor organizations have labor organization blanket bonds with a safety net rider that ensures coverage in case of a loss based upon 10% of the amount of funds handled, as determined by the latest LM report.

|

Line # |

Detail |

Amount |

LM-3 Item # |

|---|---|---|---|

|

1 |

Liquid Assets as of the start of the fiscal year |

|

|

|

1A |

Cash on hand and in banks |

$ |

25A |

|

1B |

Accounts Receivable and Other Liquid Assets |

$ |

30A |

|

1C |

Loans Receivable |

$ |

26A |

|

1D |

U.S. Treasury Securities (Market Value) |

$ |

27A |

|

1E |

Other Investments (Market Value) |

$ |

28A |

|

2 |

Total Liquid Assets (Sum of Lines 1A through 1E above) |

$ |

|

|

3 |

Receipts during the fiscal year |

$ |

44 |

|

4 |

Total Liquid Assets plus Receipts (Line 2 plus Line 3) |

$ |

|

|

5 |

Deduct Receipts included in Line 3 which resulted from converting Liquid Assets held at the beginning of the year |

|

|

|

5A |

Payments received on Accounts Receivable in Item 30A |

$ |

43 |

|

5B |

Payments received on Loans Receivable in Item 26A |

$ |

43 |

|

5C |

Sales of U.S. Treasury Securities in Item 27A |

$ |

42 |

|

5D |

Sales of Other Investments in Item 28A |

$ |

42 |

|

5E |

Sales of Other Liquid Assets held in Item 30A |

$ |

42 |

|

6 |

Total deductions (Lines 5A through 5E above) |

$ |

|

|

7 |

Total funds handled during fiscal year (Line 4 minus Line 6) |

$ |

|

|

8 |

Amount of bonding required (Line 7 times 10%) |

$ |

|

|

9 |

Maximum Amount recoverable on union’s bond (Item 20) |

$ |

20 |

|

10 |

Are you adequately bonded? If Line 9 is greater than Line 8, you areadequately bonded; but if Line 8 is greater than |

|

|

6. Properly Reconcile Cash:

The cash reconciliation process verifies the cash balance at the end of the year. This includes the addition of all receipts and the subtraction of all disbursements occurring during the course of the fiscal year. EFS will automatically reconcile end of year cash, and if cash does not reconcile, EFS will advise you. You must either review the receipts, disbursements and cash items to determine the error or provide an adequate explanation as to the reconciliation difference in Item 56. EFS validation cannot be completed unless cash can be reconciled or an explanation provided.

Although EFS assists in correcting and detecting common reporting errors, such as cash reconciliation, the following worktable may be used to determine that the figures for receipts, disbursements, and cash are correctly reported on your organization’s Form LM-3:

| Line | Receipts, Disbursements and Cash | Amount |

|---|---|---|

|

A. |

Cash at Start of Reporting Period – |

|

|

|

Item 25, Column (A) |

$ |

|

B. |

Add: Total Receipts – Item 44 |

$ |

|

C. |

Total of Lines A and B |

$ |

|

D. |

Subtract: Total Disbursements – |

|

|

|

Item 55 |

$ |

|

E. |

Cash at End of Reporting Period – |

|

|

|

Item 25, Column (B) |

$ |

If Line E does not equal the amount reported in Item 25, Column (B), then there is an error in your organization’s report which should be corrected.

If outside accountants prepare your union’s Form LM-3, we recommend you share this Compliance Tip with them. If you have any questions, please email us at OLMS- Public@dol.gov or contact your nearest OLMS field office below.

Last Updated: 11-08-18