Financial security in retirement doesn’t just happen. It takes planning and commitment and, yes, money.

Facts

- Only about half of Americans have calculated how much they need to save for retirement.

- In 2022, more than a quarter of private industry workers with access to a defined contribution plan (such as a 401(k) plan) did not participate.

- The average American spends roughly 20 years in retirement.

Putting money away for retirement is a habit we can all live with.

Remember…Saving Matters!

1. Start saving, keep saving, and stick to your goals

If you are already saving, whether for retirement or another goal, keep going! You know that saving is a rewarding habit. If you're not saving, it's time to get started. Start small if you have to and try to increase the amount you save each month. The sooner you start saving, the more time your money has to grow (see the chart below). Make saving for retirement a priority. Devise a plan, stick to it, and set goals. Remember, it's never too early or too late to start saving.

2. Know your retirement needs

Retirement is expensive. Experts estimate that you will need 70 to 90 percent of your preretirement income to maintain your standard of living when you stop working. Take charge of your financial future. The key to a secure retirement is to plan ahead. Start by requesting Savings Fitness: A Guide to Your Money and Your Financial Future and, for those near retirement, Taking the Mystery Out of Retirement Planning. (See back panel to order a copy.)

3. Contribute to your employer’s retirement savings plan

If your employer offers a retirement savings plan, such as a 401(k) plan, sign up and contribute all you can. Your taxes will be lower, your company may kick in more, and automatic deductions make it easy. Over time, compound interest and tax deferrals make a big difference in the amount you will accumulate. Find out about your plan. For example, how much would you need to contribute to get the full employer contribution and how long would you need to stay in the plan to get that money.

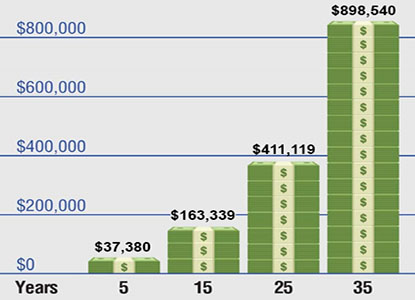

THE ADVANTAGE OF STARTING EARLY

Start Now! This chart shows what you would accumulate at 5, 15, 25 and 35 years if you saved $6,500 each year and your money earned 7% annually.

4. Learn about your employer's pension plan

If your employer has a traditional pension plan, check to see if you are covered by the plan and understand how it works. Ask for an individual benefit statement to see what your benefit is worth. Before you change jobs, find out what will happen to your pension benefit. Learn what benefits you may have from a previous employer. Find out if you will be entitled to benefits from your spouse's plan. For more information, request What You Should Know about Your Retirement Plan. (See back panel for more information.)

5. Consider basic investment principles

How you save can be as important as how much you save. Inflation and the type of investments you make play important roles in how much you'll have saved at retirement. Know how your savings or pension plan is invested. Learn about your plan's investment options and ask questions. Put your savings in different types of investments. By diversifying this way, you are more likely to reduce risk and improve return. Your investment mix may change over time depending on a number of factors such as your age, goals, and financial circumstances. Financial security and knowledge go hand in hand.

6. Don't touch your retirement savings

If you withdraw your retirement savings now, you'll lose principal and interest and you may lose tax benefits or have to pay withdrawal penalties. If you change jobs, leave your savings invested in your current retirement plan, or roll them over to an IRA or your new employer's plan.

7. Ask your employer to start a plan

If your employer doesn't offer a retirement plan, suggest that it start one. There are a number of retirement saving plan options available. Your employer may be able to set up a simplified plan that can help both you and your employer. For more information, request a copy of Choosing a Retirement Solution for Your Small Business. (See back panel for more information.)

8. Put money into an Individual Retirement Account

You can put up to $6,500 a year into an Individual Retirement Account (IRA); you can contribute even more if you are 50 or older. You can also start with much less. IRAs also provide tax advantages.

When you open an IRA, you have two options – a traditional IRA or a Roth IRA. The tax treatment of your contributions and withdrawals will depend on which option you select. Also, the after-tax value of your withdrawal will depend on inflation and the type of IRA you choose. IRAs can provide an easy way to save. You can set it up so that an amount is automatically deducted from your checking or savings account and deposited in the IRA.

9. Find out about your Social Security benefits

On average, Social Security retirement benefits replace 40 percent of pre-retirement income for retirement beneficiaries. The amount of your wages that Social Security retirement benefits replace varies depending on your earnings and the age you choose to start receiving benefits. You may be able to estimate your benefit by using the retirement estimator on the Social Security Administration's website. For more information, visit their website or call 1-800-772-1213.

10. Ask Questions

While these tips are meant to point you in the right direction, you'll need more information. Read our publications listed on the back panel. Talk to your employer, your bank, your union, or a financial adviser. Ask questions and make sure you understand the answers. Get practical advice and act now.

For More Information:

Visit the Employee Benefits Security Administration's website to view the following publications:

- Savings Fitness: A Guide to Your Money and Your Financial Future

- Taking The Mystery Out of Retirement Planning

- What You Should Know About Your Retirement Plan

- Filing a Claim for Your Retirement Benefits

- Women and Retirement Savings

- Retirement Toolkit

- Choosing a Retirement Solution for Your Small Business

To order copies, contact EBSA electronically or by calling toll free 1-866-444-3272.

The following websites can also be helpful:

American Savings Education Council

Certified Financial Planner Board of Standards

Consumer Federation of America